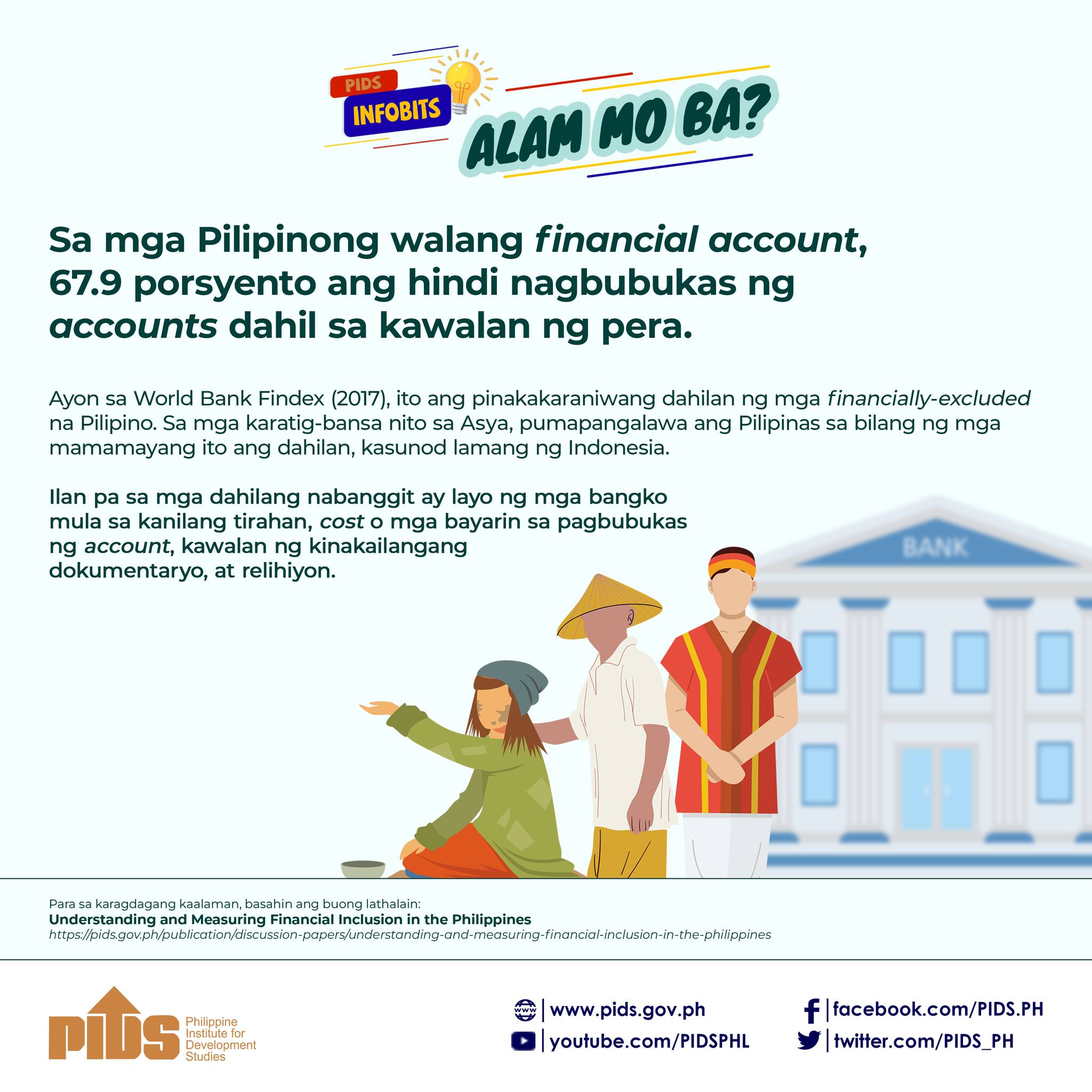

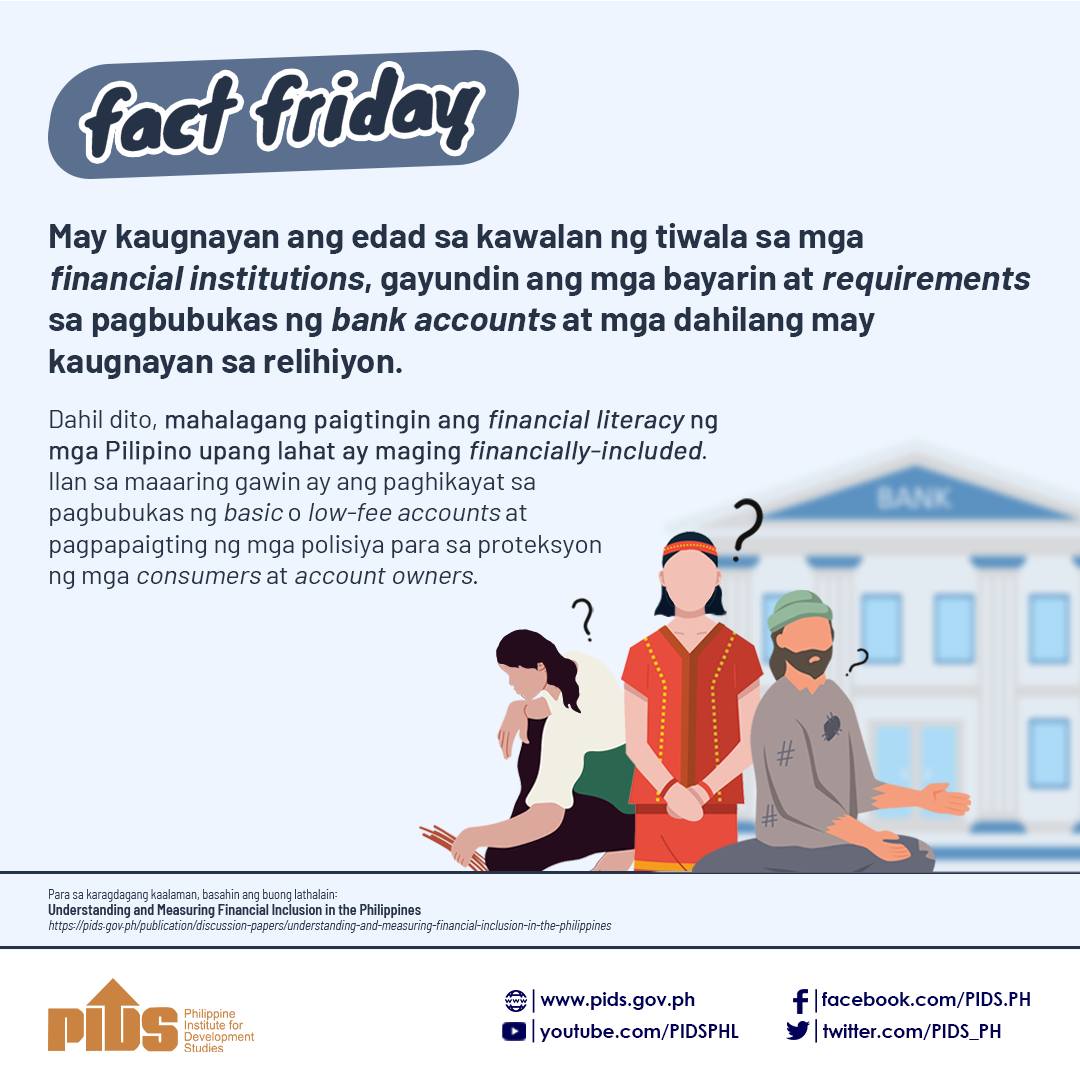

Financial inclusion can help curb poverty, reduce inequality, and potentially enhance productivity and long-term growth. However, empirical research on financial inclusion remains limited, particularly at the country level. To fill this gap, this paper conducts an empirical exploration of financial inclusion in the Philippines. Its specific objectives are to: (1) benchmark financial inclusion in the Philippines versus other countries in developing Asia; (2) capture stylized facts about financial inclusion in the country based on analysis of demand-side data; and (3) construct a subnational financial inclusion index that can be used, moving forward, to estimate the links of financial inclusion with economic growth, development, and financial stability. The Philippines leads comparator countries in terms of the enabling environment, has mixed performance in financial outreach, and lags in financial account ownership and usage. Less than 15 percent of adults in the country save money using a formal account, while less than a tenth use formal credit, among the lowest proportions in the region. In terms of stylized facts, we find that greater education, higher income, being female, being employed, and being older (up to a certain point) make financial inclusion, particularly formal account ownership and credit use, more likely. Fintech in the form of mobile money appears promising with seemingly the most equitable access among the different forms of financial inclusion, although account ownership remains scant and limited to more urbanized areas. Individuals with less education and those coming from lower-income households are more likely to be “involuntarily” excluded from the formal financial sector. To construct a subnational financial inclusion index, this paper makes use of supply-side data on outreach and usage of financial services in Philippine regions, with weights derived via principal component analysis. The computed regional index is positively associated with GDP per capita, literacy, and electricity access, and negatively associated with poverty incidence, in line with the demand-side analysis and reasonable expectations about the relationship between financial inclusion and development indicators.

Comments to this paper are welcome within 60 days from the date of posting. Email publications@pids.gov.ph

Citations

This publication has been cited 1 time

- Lawrence Agcaoili . 2021. Financial inclusion seen to ease poverty. Philippine Star.